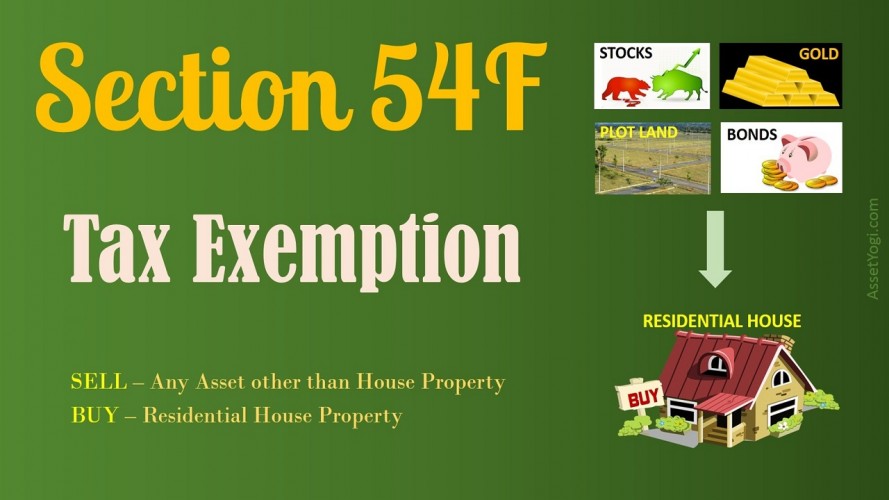

Section 54F of Income Tax Act 1961 – Decoded!

Section 54F of Income Tax Act 1961 provides for tax exemption on capital gains that result from sale of any Long Term Asset (original asset) other than Residential House Property provided that the entire net consideration is invested in 1. Purchase of one residential house property (new asset) within 1 year before or 2 years […]

Section 54F of Income Tax Act 1961 – Decoded! Read More »